Case Study: SEC Challenge of Reverse-Merger Share Price

Use of Third-Party Valuation vs. Trading Price of Public Shell

Use of Third-Party Valuation vs. Trading Price of Public Shell

At the time of the reverse-merger transaction (the “Transaction”), the Company was trading at an overstated share price ($1.50 per share). The Company’s share price had increased 5x over the year prior to the Transaction closing while the operations of the Company had not improved, and the future expectations had not changed, aside from the anticipated Transaction.

Our findings indicated that the Company was part of an inactive and inefficient market; the share price was not based on the fundamentals of the Company and did not represent its true intrinsic value. This was based on the following factors: 1,2,3,4

-

-

- The Company was traded on the most speculative tier of the three over-the-counter (OTC) marketplaces.

- The Company historically very low asset

- The Company had a small number of

- Historically there was a large bid-ask

- Historically there was a low daily dollar volume of trades.

- There was no research or analysis performed on the stock.

- No reporting institutions or institutional investors were active in acquiring shares.

-

___________________________

- 1 https://www.marketwatch.com/story/thinly-traded-stocks-proceed-with-caution

- 2 https://www.investopedia.com/terms/t/thinly-traded.asp

- 3 https://tradingsim.com/blog/5-challenges-trading-thinly-traded-stocks/

- 4 Empirical Analysis of Liquidity Demographics and Market Quality for Thinly-Traded NMS Stocks, Office of Analytics and Research, Division of Trading and Markets, U.S. Securities and Exchange Commission, April 10, 2018.

A summary of these individual factors is presented in the following section of this whitepaper. Then a discussion of ASC 820 Fair Value Measurement is included. Finally, we discuss relevant court cases and their findings on market efficiencies.

Summary of Findings

-

OTC Exchange Listing

As of the Closing Date, the Company’s shares were traded on the OTC Pink marketplace, which is the most speculative tier of the three OTC marketplaces.

-

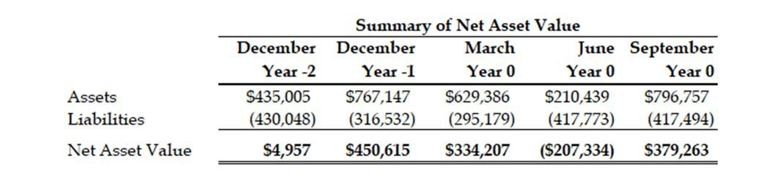

Low Asset Value

Prior to assets being transferred into the public shell, the Company held few assets. For a two- year period prior to the transaction, the Company had very few assets with net asset value under $500,000 (and negative for some periods). This indicates the Company had little, if any, operations prior to the Transaction. A summary of the Company’s net asset value prior to the closing date is presented in the figure below (closing date year is year 0).

In fact, over that time period, the Company’s going concern status was in flux, as auditors considered whether the Company had the ability to continue as a going concern.

-

Small Number of Shareholders

As of the closing date, the Company had 18+ million shares outstanding with less than 400 unique shareholders. Bloomberg showed the Company had a float of around 1 million shares; however, this is an estimate. Immediately prior to the Transaction, the number of shares held by the stock transfer company was roughly 300,000. This was an extremely small number of shares available for active trading and represented less than 2% of the total outstanding shares at that time. This indicated that the Company’s stock was thinly-traded, highly volatile, and susceptible to speculative price swings.

-

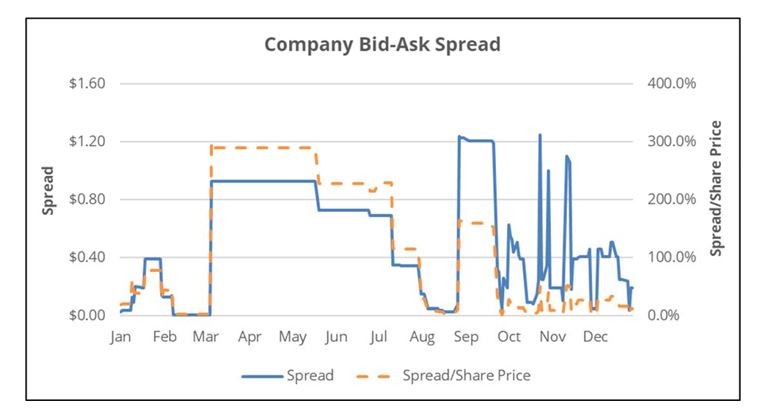

Large Bid-Ask Spread

The difference between the bid and ask price is usually indicative of a security’s liquidity. Thinly traded securities have a wider bid-ask spread than liquid securities. For the fiscal year prior to the Transaction, the Company had an average bid-ask spread of roughly $0.50 with a maximum of $1.25. In fact, for large periods, the bid-ask spread was over two times as large as the Company’s actual share price. Assets considered less liquid typically have spreads equivalent to 1%-2% of the asset’s stock price.5 This indicated that the Company was very thinly traded and susceptible to speculative price swings.

The following chart presents the Company’s bid-ask spread over the year prior to closing.

-

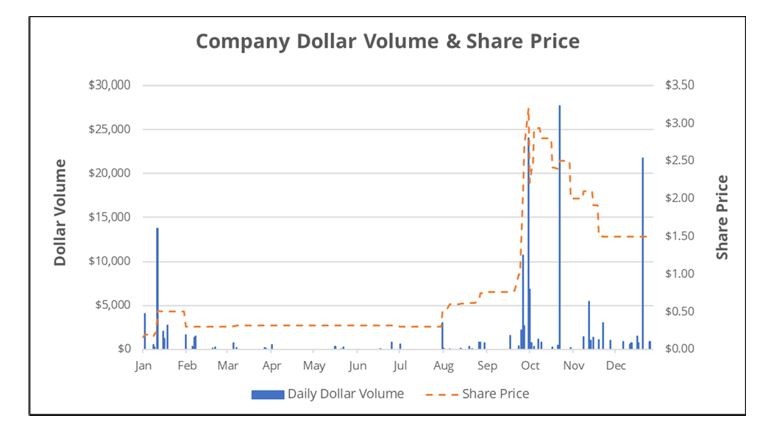

Low Daily Dollar Volume of Trades

The Company had a very low daily dollar volume of trades. From the year prior to the Transaction, the Company averaged roughly $600 in trades a day (251 total days). In fact, the majority of days (189 days) had zero trades occur. Only on three days did the dollar volume go above $20,000. This indicated that the Company was not in an actively traded market with significant investor interest. The inefficient market meant that trades were not being executed due to newly available or disseminated corporate information.

The chart below presents the Company’s daily dollar volume of trades and share price.

______________________

5 https://www.investopedia.com/terms/b/bid-askspread.asp

-

No Research or Analysis Performed on the Stock

We searched Bloomberg and S&P Capital IQ for any research or analysis performed on the Company prior to the closing date. We found no reports relating to the Company. Reports were not created until after the closing date. This indicated that any trades occurring prior to the closing date were speculative and not based on the fundamentals of the Company.

-

No Reporting Institutions or Institutional Investors Acquiring Stock

Trades of the Company stock prior to the Transaction were made by individual, speculative investors. There was no evidence that reporting institutions or institutional investors were buying the Company’s stock.

ASC 820 – Fair Value Measurement

We also looked to ASC 820 Fair Value Measurement for guidance on inactive markets.

ASC 820-10-35-54C through 35-54H addresses valuations in markets that are inactive in the current reporting period.6

_______________________

6 Language in this section was paraphrased from PwC’s Fair Value Measurements Guide, dated August 2015.

The fair value standards provided additional factors to consider in measuring fair value when there is low market activity for an asset or a liability and quoted prices are associated with transactions that are not orderly. For those measurements, pricing inputs for referenced transactions may be less relevant. A reporting entity should determine if a pricing input for an inactive security was “orderly” and representative of fair value by assessing if it has the information to determine that the transaction is not forced or distressed. If it cannot make that determination, the input needs to be considered.

This ASC provides a list of factors to consider in determining whether the volume or level of activity is in relation to normal market activity. The factors that an entity should evaluate include, but are not limited to, the following:

-

-

- There is an absence of a market for new issues (that is, a primary market) for that asset or liability or similar assets or liabilities – the Company was not traded on a primary

- There is an absence of a market for new issues (that is, a primary market) for that asset or liability or similar assets or liabilities – the Company was not traded on a primary

-

-

-

- There are few orderly transactions – the Company had no, or very few, orderly

- There are few orderly transactions – the Company had no, or very few, orderly

-

-

-

- Price quotations are not developed using relevant or current information – the Company had issued no relevant or current information that could be used to develop a price quotation.

- Price quotations are not developed using relevant or current information – the Company had issued no relevant or current information that could be used to develop a price quotation.

-

-

-

- Price quotations vary substantially either over time or among market makers (for example, some brokered markets) – the Company had no market makers or any brokered markets.

- Price quotations vary substantially either over time or among market makers (for example, some brokered markets) – the Company had no market makers or any brokered markets.

-

-

-

- There is a wide bid-ask spread or significant increases in the bid-ask spread – Wide bid- ask spreads were the norm for the Company.

- There is a wide bid-ask spread or significant increases in the bid-ask spread – Wide bid- ask spreads were the norm for the Company.

-

-

-

- Little information is publicly available (for example, a principal-to-principal market) – There were no principal-to-principal markets for the Company or any other publicly available information prior to the transaction.

- Little information is publicly available (for example, a principal-to-principal market) – There were no principal-to-principal markets for the Company or any other publicly available information prior to the transaction.

-

If a reporting entity concludes that the volume or level of activity in the market for an asset or liability is low, the reporting entity should perform further analysis of the transactions or quoted prices observed in that market. Further analysis is required because the transactions or quoted prices may not be determinative of fair value, and significant adjustments may be necessary when using the information in estimating fair value. ValueScope performed this analysis as presented above in the Summary of Findings Items 1 through 7.

The fair value standards do not prescribe a methodology for making significant adjustments to transactions or quoted prices when estimating fair value. Instead of applying a prescriptive approach, reporting entities should consider indications of fair value.

For example, a reporting entity may use indications of fair value developed from both a market approach and a present value technique in its estimate of fair value. When using multiple indications of fair value, the reporting entity should consider the reasonableness of the range of fair value indications. The objective is to determine the point that is most representative of fair value under current market conditions.

In inactive markets, market capitalization may not be representative of fair value, and other valuation methods may be required to measure the fair value of an entity. Use of a value other than market capitalization will require other evidence and documentation that clearly support that the quoted market prices are not the best indication of fair value. This guidance is set out in ASC 820-10-35.

Relevant Court Cases

Cammer v. Bloom

In the Cammer v. Bloom opinion, five factors are presented that determine whether the market for a security is efficient. These include the following:

-

-

- Trading volume

- Coverage by securities analysts

- Number of market makers

- Eligibility for S-3 registration

- Empirical evidence that the security price reacts to new, company-specific information

-

In the case of the Company, none of these factors were present, indicating that the market for the Company’s stock was inefficient.

Krogman v. Sterritt

The Krogman v. Sterritt case identified three additional factors that are also indicative of market efficiency (these factors have since been considered by other courts, including in the Second Circuit regarding Petrobras). These include the following:

-

-

- The company’s market capitalization

- The security’s float

- The typical bid-ask spread for the security

-

As discussed previously, the Company had a small market capitalization and float and a large bid-ask spread. This also indicated that the market for the Company’s security was inefficient.

Conclusion

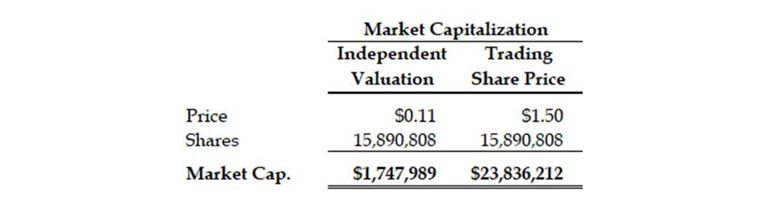

ValueScope reviewed the characteristics of the Company prior to the reverse-merger transaction and found that the trading price was not indicative of the fundamentals of the Company. A comparison of the market capitalization of the Company based on the different share prices considered in this case is presented in the table below.

At the trading price as of the closing date ($1.50 per share), the Company is extremely overvalued. A public shell company with declining operations and low asset value would not have a market capitalization of nearly $24.0 million. The Company was part of an inactive and inefficient market, and the share price did not represent the true intrinsic value of the Company. We found the following factors led to this conclusion:

-

-

- The Company was traded on the most speculative tier of the three over-the-counter (OTC) marketplaces.

- The Company maintained historically a very low asset

- The Company had a small number of

- Historically, there was a large bid-ask

- Historically, there was a low daily dollar volume of

- There was no research or analysis performed on the

- No reporting institutions or institutional investors were active in acquiring

-

ASC 820-10-35-54C through 35-54H support our conclusion that the Company did not have an active trading market prior to the Transaction. Furthermore, relevant court cases such as Cammer v. Bloom and Krogman v. Sterritt provide their own factors for market efficiency. The Company’s stock, as of the closing date, met none of these factors, thereby backing up our own findings. The independent valuation of the Company’s stock ($0.11 per share) was the most indicative measure of intrinsic value and reflected the fundamentals of the Company more so than the trading share price.

ValueScope: Measuring, Defending and Creating Value for Our Clients

ValueScope is a leader in the application of fair value measurement applying the Mandatory Performance Framework for better compliance with the Public Company Accounting Oversight Board.

For more information or to contact us for any need you may have, please feel free to write or call. We look forward to speaking with you.

ValueScope Inc.

- Steven C. Hastings, CPA/ABV/CFF, CGMA, ASA, CVA

- (Office) 817-481-4901

- shastings@valuescopeinc.com