Executive Summary

The Issue:

Companies are facing cash shortfalls as they struggle to reopen from the COVID-19 lockdown. Companies facing short-term liquidity challenges can seek new cash sources, such as the government’s Payroll Protection Program “PPP” or a bank line-of-credit. However, certain companies may never achieve the revenue and profitability necessary to remain viable as a going-concern and may ultimately be forced into bankruptcy. Understanding whether your company faces a liquidity or solvency issue will allow you to most efficiently utilize your available resources.

Illiquid vs. Insolvent

Operating models of illiquid companies may be viable in the long-term, but cash issues could arise in the near-term due to poor cash management or an exogenous shock to the company’s operating performance. Insolvent companies, on the other hand, have an unsustainable operating model to support operating and debt obligations over the long-term.

What Needs to be Done?

A complete understanding of the company’s financial obligations and operating outlook is necessary to understand whether the company is experiencing a liquidity or solvency issue. Companies which are publicly traded or have bank debt may require solvency opinions to be performed. ValueScope’s team of experienced financial analysts and consultants can help you understand what your options are to get through this difficult time.

Our team of professionals provides:

-

- Experience- we’ve conducted solvency and liquidity analyses for clients across the country

- Credibility- Ph.D.’s, CFA’s, CPA’s, ASA’s, CVA’s, and MBA’s

- Independence- we have the personnel, expertise and research resources to provide the assurance you require for a solvency opinion

The Issue at Hand

As businesses have been unable to fully function because of the COVID-19 pandemic, governments have stepped in to provide stimulus packages to equip them with the resources to survive the short-term. In the United States, the Payroll Protection Program (“PPP”) was set up to provide small businesses with a direct financial incentive to keep their workers on the payroll [1]. Yet the PPP, or any realistic government program, can only solve a business’s short-term liquidity issues. When a business’s operating performance struggles for a prolonged period of time, and their short and long-term cash inflows are no longer able to meet their financial obligations, the company could become insolvent.

Understanding a Liquidity Issue

A company’s liquidity is a measure of its ability to meet its near-term financial obligations. Companies can be profitable with positive cash flow and experience liquidity issues.

As an example, assume ABC Company has the following cash flow statement:

As the cash flow statement indicates, ABC Company has positive monthly net income of $100, and sufficient cash flow to cover their necessary capital expenditures and debt repayment obligations. As a result, the net monthly cash flow is positive $50. However, a profitable company can still experience a short-term liquidity issue.

As mentioned above, liquidity issues arise when a company cannot meet their near-term financial obligations. Imagine that ABC Company has the following balance sheet:

Companies experiencing a liquidity problem often face a disconnect between their current assets and current liabilities. As the ABC Company balance sheet indicates, the company’s current ratio is below 1.0, meaning current liabilities exceed current assets [2, 3].

Additionally, assume $50 of the salaries payable are due today and $25 of the short-term debt is due tomorrow. Currently ABC Company’s cash on hand is insufficient to meet these needs. ABC Company is now unable to meet their debt obligations and could be forced into bankruptcy if they cannot meet their obligations.

Dealing with Liquidity Issues

Fortunately, liquidity issues can be resolved in the short-term through obtaining additional financing, such as a line of credit, and in the long-term through better cash flow management. Improved cash flow management could include negotiating better terms on a company’s AR and AP, and better managing inventory levels.

The PPP is designed to keep companies from experiencing liquidity issues by providing them with the cash necessary to pay their day-to-day expenses and keep them from experiencing a liquidity issue. However, the PPP is not indefinite, in which case businesses which struggle to regain their customers could ultimately experience a solvency issue.

Understanding When Illiquid Becomes Insolvent

While there are numerous operational and financial options for companies experiencing illiquidity issues, companies experiencing insolvency have far fewer options. Insolvency includes illiquidity, but without realistic financing options and immediate operational opportunities for improvement.

As an example, assume that XYZ Company has the following cash flow statement:

Unlike our illiquid company, XYZ Company’s monthly cash flow is not sufficient to cover their debt repayment obligations. Even if they were to cut their capital expenditures to $0, XYZ Company would not generate sufficient cash flow to service their debt. In this scenario, any short-term financing or accounts receivable improvement would only provide a temporary solution.

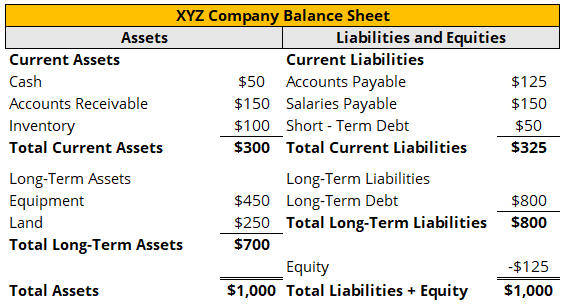

Additionally, imagine the XYZ Company has the following balance sheet:

In addition to having cash flow issues, XYZ Company also has total liabilities which exceed total assets. Between their short-term and long-term debt, XYZ Company has total debt of $850. Even if XYZ Company sold all of their assets at book value, they would not be able to cover their debt obligations.

Dealing with Insolvency

Companies facing insolvency do not generate the income and cash flow necessary to support their operational and debt obligations. These companies must identify opportunities to increase net income and cash flow from operations, either through increasing revenue or decreasing expenses. If the company is unable to improve their operations, their debt burden will be too great, and the company will eventually be forced into bankruptcy.

ValueScope Can Assist You

Companies facing liquidity and solvency issues face tremendous challenges. Whether it is dealing with creditors, requiring solvency opinions, or working to improve cash flow management, ValueScope’s team of financial and valuation consultants can assist you and help get you through this difficult time.

[1] Loans made through the PPP will be forgiven if all employees are kept on staff for the next eight weeks and the money is used for payroll, rent, mortgage interest, and utilities. (Source: https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/paycheck-protection-program-ppp)

[2] Current Ratio = Current Assets / Current Liabilities. The current ratio is the most basic liquidity test. It signifies a company’s ability to meet its short-term liabilities with its short-term assets. A current ratio greater than or equal to one indicates that current assets should be able to satisfy near-term obligations. A current ratio of less than one may mean the firm has liquidity issues. (Source: Morningstar).

[3] Evaluating a “good” current ratio requires a review of the business model, industry averages, and historical performance.

[4] Currently the PPP funds must be spent in the first eight weeks for the loan to be forgiven.

For more information, contact:

Benjamin Westcott, CFA

MANAGER

Full Bio →

The information presented here is not nor should it be treated as investment, financial, or tax advice and is not intended to be used to make investment decisions.

If you liked this blog you may enjoy reading some of our other blogs here.